FAQs

Business Protection

Professional Indemnity

Do I need professional indemnity insurance?

If you provide advice, designs, or professional services, you should strongly consider professional indemnity insurance. Without it, you could face costly legal fees and compensation claims if a client accuses you of negligence.

Additionally, many clients require professional indemnity insurance before entering into contracts, and industry associations may have minimum coverage requirements for membership.

What types of claims does professional indemnity insurance cover?

Professional indemnity insurance protects against a wide range of claims, including:

- Management consultants – A business plan you provide doesn’t deliver expected results, and the client claims for financial losses.

- IT contractors – A website, app, or software is not fit for purpose, and the client claims for rectification costs.

- Engineering contractors – CAD work contains incorrect measurements, delaying a project, and the client claims for extra expenses.

- Fitness professionals – A client sustains an injury and claims that you failed to properly instruct them.

- Photographers – A client is dissatisfied with your work, or images are lost due to technical failure, leading to a claim for reshoot costs.

- Tutors – A student fails to achieve expected grades and claims for financial losses related to missed opportunities.

Can I get proof of cover for a contract?

Yes. Your insurance provider will issue a Confirmation of Liability Insurance document or similar, which you can present to clients and agencies as proof of coverage.

Do you offer short-term professional indemnity policies?

No, most professional indemnity policies run for 12 months, and for good reason.

Professional indemnity insurance operates on a ‘claims made’ basis – meaning:

- Your policy must be active both at the time of the alleged incident and when the claim is reported.

- If you cancel your policy and a past client makes a claim, you won’t be covered.

Maintaining continuous cover ensures protection for work completed in previous contracts.

How much professional indemnity cover do I need?

Check if your client or industry regulator requires a minimum level of cover.

If no minimum is specified, consider worst-case scenarios and the potential costs of rectifying a mistake. iPro, our preferred partner, offers coverage between £50,000 and £5 million, ensuring the right protection for your business.

What is cyber protection insurance?

Cyber protection insurance helps businesses recover from cyberattacks, data breaches, and system failures. It typically covers:

- Financial losses due to hacking, ransomware, or data theft.

- Legal and regulatory costs associated with data breaches.

- Notification and credit monitoring for affected customers.

- IT forensics and recovery services to restore compromised systems.

Do small businesses need cyber insurance?

Yes. Small businesses are increasingly targeted by cybercriminals due to limited cybersecurity resources. Cyber insurance helps mitigate risks, ensuring financial and operational protection against cyber threats.

What is public liability insurance?

Public liability insurance covers injuries or property damage caused by your business operations. If a customer, supplier, or member of the public is injured or their property is damaged due to your business activities, this insurance covers legal fees and compensation claims.

Who needs public liability insurance?

Any business that interacts with clients, customers, or the public should have public liability insurance. This includes:

- Retailers

- Tradespeople (electricians, plumbers, builders)

- Event organizers

- Freelancers working in public spaces

What is retroactive cover?

This cover provides extra protection for work your business carried out prior to the policy inception date. Unless you specifically request retroactive cover (and provide us with a date to ‘back-date’ your cover to), the policy will only cover work carried out from the inception date of your policy.

The reasons you may want to backdate your cover are; to ensure that you’re covered for work and contracts you have previously entered, or are currently engaged in, and because it could be many months or even years before you are aware of a potential claim arising from work carried out in the past. For example, it might be some time before your client realises they are unhappy with the service you provided.

Shareholder Protection

How is shareholder protection structured?

There are three main ways to set up shareholder protection:

- Own life plans under business trusts – Each shareholder takes out a policy on their own life, written in trust for the benefit of other shareholders.

- Life of another plans – Each shareholder owns policies on the lives of other shareholders.

- Company-owned plans – The company takes out policies on shareholders to fund the buyback of shares.

Speak to your Broadbench financial adviser to determine the best option for your business.

What is a cross-option agreement?

Also known as a double-option agreement, this gives surviving shareholders the option to buy shares from the deceased shareholder’s personal representatives.

- If either party wishes to exercise their option, the other must comply.

- The option can only be exercised after death, within a specific timeframe.

Does a cross-option agreement affect IHT business property relief?

No. If a shareholder passes away while owning shares in an unquoted trading company, 100% Business Property Relief (BPR) may apply for inheritance tax (IHT) purposes, as long as the shares were held for at least two years.

Even if the estate receives cash for shares under a cross-option agreement, BPR is preserved because:

- The option is only exercisable after death.

- There is no binding contract to sell at the time of death.

What happens if shareholders enter into a buy/sell agreement?

A buy/sell agreement would deny Business Property Relief.

- Shareholders agree that, upon the death of one, the remaining shareholders must buy their shares, and the estate must sell.

- Life insurance is taken out to fund the purchase.

Since this creates a binding contract at the time of death, HMRC treats the shares as already converted into cash, making them fully subject to IHT.

How does critical illness affect shareholder protection?

A critically ill shareholder may be unable to contribute to the business and may want to exit. Their co-shareholders will need funds to buy their shares.

- If a business trust is used, a policy with critical illness cover can be written under the trust.

- Instead of a cross-option agreement, a single-option agreement is recommended. This ensures that a critically ill shareholder is not forced to sell against their wishes.

A forced sale could trigger capital gains tax (CGT) and future IHT liabilities, as the shareholder would receive cash instead of retaining shares that may qualify for IHT Business Property Relief.

What happens if the single option is not exercised?

If a shareholder receives a critical illness payout but chooses not to sell their shares, we recommend keeping the proceeds within the trust until the succession issue is resolved.

Although the funds might be available, they were intended for share buyout purposes. Distributing them to the critically ill shareholder could lead to tax complications.

Are there disadvantages to leaving proceeds in trust?

Yes, there is a potential Pre-Owned Asset Tax (POAT) charge.

POAT is an income tax charge applied when someone benefits from an asset they previously owned. While Business Trusts used for shareholder protection fall under POAT, in most cases, the annual benefit remains below the £5,000 tax-free limit.

- The charge is 2% of the open market value of the life plan (subject to official rate changes).

- While the insured person is healthy, the market value is low, meaning no charge applies.

- If they become critically ill and the funds remain in trust, the value increases, potentially triggering POAT.

To avoid this, the settlor (original policyholder) can be removed as a beneficiary of the trust. However, this may have IHT implications, which should be reviewed with a Broadbench adviser.

Business Loan Protection

How do you take out business loan protection?

When a business takes out a loan, a specific shareholder(s) is usually responsible for repayment. Business loan protection is taken out on the individual responsible for the repayments. If the business is a limited company, the business itself is the policyholder. In the case of a partnership or sole trader, the individual owners hold the policy.

Our expert advisers can help tailor a policy to fit your business needs.

Is business loan insurance and key person insurance the same thing?

Not exactly. While key person insurance can sometimes be used to cover business loan repayments, there are key differences:

- Business loan insurance must match the outstanding loan amount to ensure full coverage of repayments.

- It must be in place for the duration of the loan, whereas key person insurance covers the length of a key individual’s employment.

What can business loan insurance cover?

Business loan insurance can cover various types of loans, including:

- Commercial loans or mortgages on business premises

- Venture capital loans taken during startup or expansion

- Director’s loans—funds paid to a director or their family that do not count as salary or dividends

Do you need to take out business loan protection?

No, there is no legal requirement to take out business loan protection.

However, lenders often require businesses to provide security to guarantee loan repayment, making business loan protection a highly recommended safeguard.

Can business loan insurance be transferred if the loan is refinanced?

Yes, in many cases, business loan insurance can be adjusted or transferred to cover a refinanced loan, as long as the coverage aligns with the new loan amount and terms.

What happens if the insured person leaves the business?

If the person covered by the business loan insurance leaves the company, the policy may need to be restructured or reassigned to a new individual responsible for the loan repayments. Our advisers can help ensure continuous coverage in such cases.

Business Healthcare

How much does small business health insurance cost?

The cost varies based on several factors, including:

- Number of employees

- Company location

- Employee ages and family status

- Underwriting type, which depends on whether you already have health insurance coverage

Coverage options, excess levels, and hospital choices can be customized to fit your employees’ needs.

Is health insurance a business expense?

Yes. If you’re a director of a limited company or a sole trader, you may be able to claim business health insurance as a tax-deductible expense.

To qualify, ensure you purchase a business health insurance plan, not a personal health insurance plan, as personal policies may not be eligible for tax deductions.

How do I get health insurance for my small business?

Our expert advisers can help tailor a policy that meets your business needs. Contact us to discuss your options.

What does small business health insurance cover?

Coverage depends on your policy but can include private hospital treatment, specialist consultations, diagnostic tests, and mental health support. Some plans may also offer dental and optical care.

Can I cover family members of employees under a business health insurance plan?

Yes, many business health insurance plans allow employees to add family members at an additional cost. This can be a valuable employee benefit.

What happens if an employee leaves the company?

If an employee leaves, they can often switch to a personal health insurance policy without needing to reapply. You can also adjust your business policy to remove them from coverage.

Executive Income Protection

How does Executive Income Protection work?

Executive Income Protection (EIP) covers an employee’s sick pay if they are unable to work due to illness or injury. The benefit is paid to the company, which then passes it on to the employee, with tax applied at that stage.

Who is the owner of an Executive Income Protection (EIP) Plan?

The policy is owned and funded by the business, not the insured individual.

How long does income protection last?

You can choose the policy duration, but it cannot extend beyond your retirement age.

What is short-term income protection?

A short-term income protection plan provides coverage for a portion of your income if you’re unable to work due to illness or injury, typically for up to 12 or 24 months per claim.

What is long-term income protection?

A long-term policy covers a portion of your income until you either return to work or the policy expires. Most plans offer coverage up to retirement age.

What is a deferral period?

The deferral period is the waiting time between becoming ill or injured and when you can start claiming benefits. Shorter deferral periods increase the cost of the policy.

For example, if you have three months of sick pay and savings to cover two additional months, a five-month deferral period may be suitable.

What is "waiver of premium"?

Waiver of premium is a feature that covers your insurance payments while you’re claiming benefits. This is typically included as standard with executive income protection.

Key Person

What is Key Person Protection?

It’s simply a business insuring itself against the financial loss it may suffer as a result of the death (or critical illness if chosen) of a key person.

Who is a key person?

A key person is an individual whose skill, knowledge, experience or leadership contributes to the continued financial success of the business. A key person may be anyone whose death could lead to a financial loss for the business.

This might be a loss of profits if you lost your best salesperson, the cost of having to recruit or train a replacement or important personal or business contracts lost due to the key person not being there to maintain a contract.

How do we prove someone is a key person?

For a business to insure one of its key people it must show that it stands to suffer a financial loss of profits as a result of the death, terminal or critical illness (if chosen) of that employee.

This is usually straightforward, and that individual is then regarded as a key person. The loss of a key person could lead to the business being unable to repay a loan, which could mean the lender calls in the loan early. This may have a serious effect on any existing loans or any future lending.

What types of companies can apply for Key Person Insurance?

Usually, a limited company or a corporation with shareholders whose liability is limited by their shareholdings. Any personal assets are held separately from the finances and assets of the company.

Who pays the premiums for Key Person Insurance?

As the company is the owner of the policy it would usually pay the premiums.

Who receives the pay-out benefits?

In the event of a valid claim, the policy proceeds would be payable to the company.

What is a partnership?

A partnership is a relationship which exists between persons carrying on a business in common with a view to profit. The partnership does not have a separate legal identity and each partner would be liable for any trade debts. It is the partners and not the partnership itself which will own any policy.

Can partners take out Key Person cover on each other?

Yes, a partner could take out their own life policy and place it under trust for the other partners. In the event of a valid claim the policy proceeds would be payable to the trustees who would in turn pay the partners as beneficiaries of the trust. The partnership would usually pay the premiums.

Can partners in Scotland take out Key Person cover on each other?

Yes. In Scotland, a partnership is a separate legal entity and can apply for the policy in its own right. The partnership applies for the policy and completes the policy owner questionnaire. In the event of a valid claim, the policy proceeds would be payable to the partnership. As the partnership is the owner of the policy it would usually pay the premiums.

What happens if the key person leaves or retires?

If a key person were to leave or retire before the end of the Key Person Protection policy term, the business could stop paying the premiums allowing the policy to lapse. Alternatively, the company may choose to continue paying the premiums until the end of the policy term and in the event of a claim, the business would receive a capital sum.

Can Key Person's cover be written in trust?

Yes, the taxation of this can be complicated, for both the company and the life insured. National Insurance, and Capital Gains tax may all need consideration. We strongly recommend that you speak to one of our specialist advisers to guide you through this.

What is the difference between Key Person Insurance and Shareholder Protection?

In many ways these are similar products, they both pay out a lump sum in the event of a claim. The major difference is where the sum assured goes in the event of a claim and the reason each was taken out.

Key Person Insurance is designed to offer a lump sum or regular monthly income cash injection into a business to mitigate any loss that would occur from either the death or long-term illness of anyone that contributes to the profit of a business.

Shareholder Insurance is slightly different in that it allows other shareholders in a business to maintain control following the death (or severe illness) of another shareholder. It helps to avoid instances where a family member of the dead shareholder can take control.

Does your business need Key Person Insurance?

If your business has anyone whose loss, either permanent or temporary would affect the company’s ability to maintain turnover and generate profit then you should explore this protection.

The number of key individuals will vary from one business to another, there is almost always at least one key person in any given business.

Who should be covered by Key Person Insurance?

The obvious choice of key person will normally be some or all of the partners or members in the business. However, it is worthwhile to consider the impact on the business of losing someone who may not have any financial stake in the business but nevertheless plays a fundamental role in its success.

Consider the individuals within your business and ask yourself:

- Would the loss of that person negatively impact or slow down any ongoing projects?

- How easy would it be to replace that person’s expertise?

- Is that individual essential to your business growth?

- Would the loss of that person detriment any customer or supplier relationships?

- Would the business miss their contribution?

- Are there any financial matters, such as bank loans that are dependent upon that key person?

If I don’t take out Key Person Insurance what are the consequences?

The consequences of losing a key person vary on the role of that individual and your business model. There are common factors to consider though, such as without the leadership of you or your key person your employees may decide it’s time for them to move on. Perhaps your customers may choose to go elsewhere and/or your sales revenue could fall. Potentially it could create a lack of confidence from your lender, suppliers, customers, and your other employees. Bank loans and overdrafts could be called in and your suppliers may demand payment upfront.

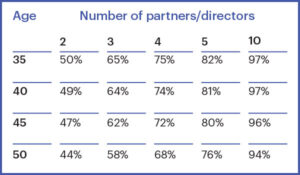

How likely is it that a Key Person will need to Claim?

Likelihood of a Critical Illness – Likelihood of at least one partner or director getting a critical illness before age 65 Source CIBT02 Based on 1971-2003 population data and experience, published in SIAS paper Exploring the critical path, 2006. Males’ standalone, extended cover, including own occupation total and permanent disability.

Likelihood of Death – Likelihood of at least one partner or director dying before age 65 Source www.actuaries.org.uk. Based on mortality data from TMNOO (temporary assured lives, male non-smokers, 1992-2002) at five plus years duration.

How much should I insure my key people for?

There are no hard and fast rules when assessing the financial value of a key person. Each key person must be dealt with on their own merits. A primary method of calculating the key person’s worth is as a multiple of the company profits, the standard multiples are 2 x gross profit or 5 x net profit.

Alternatively, some firms calculate the value as a multiple of that person’s salary. Up to ten times gross salary may be considered for a rapidly expanding business.

Your Broadbench adviser will guide you through this calculation.

What’s the tax position for Key Person Insurance?

Typically, tax relief is not allowed as in nearly all cases the key person being insured is a major shareholder of the business. Just because the policy may not qualify for tax relief does not mean that the company should not take key person insurance. It just means they will not get tax relief on the premiums.

Who do I notify in the event that a policyholder passes away?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

What do I do if the key person changes their name?

You should notify your insurer’s customer services team or your broker so that the policy details remain up to date. For Broadbench clients, you can update this information on our client portal.

The key person has moved house, how do I update their address details for my Key Person insurance policy?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

What should I do if my bank details change for my Key Person Insurance policy?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

Relevant Life

What is Relevant Life Insurance?

It’s not a nice thing to think about, but if you’re a contractor and you pass away, how would your loved ones survive? This is where Relevant Life Insurance can provide the answer. It pays out a large one-off sum to help your family live after you’ve gone. Plus, a Relevant Life policy offers some very special advantages to limited company business owners and contractors looking for life cover. The headline benefit is tax efficiency.

While the life cover is personal to you, the policy counts as a legitimate business expense, so it is tax deductible. Learn more about how a Relevant Life Policy could be suitable for you by contacting us.

Am I eligible to take out a Relevant Life Insurance policy?

You must have a limited company to benefit from the tax savings that a relevant life insurance policy offers. If you do not have a limited company then standard Life Insurance will offer you the protection you need.

Do I get any money back if I don't die before the Relevant Life Insurance policy term ends?

No. There’s no cash value at any time. Just like standard Life Insurance at the end of your Relevant Life Insurance policy term you stop making payments and your cover ends.

Can my mortgage be covered with Relevant Life Insurance?

If you have an interest-only mortgage, your outstanding mortgage loan stays the same until you repay it at the end of the mortgage term. Level Relevant Life Insurance could cover this type of mortgage.

How does Relevant Life Insurance work? What do I need to know?

Like standard Life Insurance, it provides your loved ones with a large tax-free, one-off payment, or monthly payments if you pass away. It can be used to pay the mortgage off or help your family with living expenses. You are covered only for the duration (term) of the policy and cover only lasts while you keep up monthly premiums. Monthly payments can be reduced by combining this with a Critical Illness policy.

The key difference between Life Insurance and Relevant Life Insurance is that with Relevant Life Insurance the cost of the premiums is moved from your own pocket to your company expenses. This saves you tax and reduces the cost of your monthly premiums.

Additionally, this is not treated as a benefit-in-kind; the premium is not included as a P11D benefit, nor are premiums subject to National Insurance payments for the employer or employee.

There is significant tax relief with a Relevant Life plan and your business can claim Corporation Tax Relief on the premiums. Plus, the payout itself is tax-free.

How do I know what the right policy for me is?

If the unexpected happens, you’d want your family to be taken care of. You’d want the mortgage paid off and enough money for them to live. It’s important to get this right, which is why we work closely with you, making sure the cover fits your needs but is also affordable for you. The policies we recommend are handpicked for contractors, and we’ll cut through any jargon, so you know exactly where you stand.

Will my payments on my Relevant Life Insurance policy change?

If you choose level or decreasing cover, your monthly payments are guaranteed to stay the same for the duration of your policy. For decreasing Relevant Life Insurance, premiums are set at the start of the policy to consider the decreasing amount of cover you’ll need during the policy term. Premiums for decreasing cover are often cheaper than other types of life insurance.

With level cover, if you choose to help protect your payments from the effects of inflation, so the lump sum won’t be worth less in the future, your monthly payments may rise. The maximum annual increase would be 15% to your premiums and 10% to your cover.

Who do I notify in the event that a policyholder passes away?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

What do I do if I change my name?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

I've moved house, how do I update my address details for my Relevant Life insurance policy?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

What should I do if my bank details change for my Relevant Life Insurance policy?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

Can I cancel my Relevant Life Insurance policy at any time?

Yes. You have a 14-day cooling-off period from your policy start date, or from when you get your policy documents (whichever is later), to change your mind. If you want to cancel within this time, we’ll refund any premiums you’ve paid. Remember, there’s no cash value and, if you cancel your policy, you won’t be able to make a claim.

How do I pay for my Relevant Life Insurance policy?

You can pay your premiums monthly by Direct Debit.

Is Terminal Illness Cover included in a Relevant Life Insurance policy?

Many Life Insurance policies have the option to include Terminal Illness Cover. Your Broadbench adviser will go through all of the available options with you to ensure the policy meets all of your requirements.

What is Terminal Illness Cover?

Terminal Illness Cover will pay out when you contract an illness/ disease that has no known cure or has progressed to a point where it cannot be cured, and you aren’t expected to live longer than 12 months.

What does my Relevant Life Insurance policy cover me for?

You can find out what you’re covered for in the policy documentation. If you’re not sure please contact us.

What’s Relevant Life Insurance with decreasing cover?

If you have a Relevant Life Insurance Plan with decreasing cover, the cover amount decreases over time, broadly in line with the repayment mortgage or long-term loan that you’re repaying. Your premiums stay the same during the term of the policy, unless you make changes to the cover. Decreasing cover usually costs less than level cover.

The policy will pay out if you die, or are diagnosed with a terminal illness and aren’t expected to live longer than 12 months, during the policy term. The policy only pays out once and has no cash value at any time.

What’s Relevant Life Insurance with increasing cover?

If you have a Relevant Life Insurance policy with increasing cover, the level of cover, and your monthly payments, may increase over time to help protect your cover amount from the effects of inflation.

The policy pays out a lump sum if you die during the policy term, or are diagnosed with a terminal illness and aren’t expected to live longer than 12 months. The policy will only pay out once, so if you make a successful terminal illness claim, a second claim can’t be made. There’s no cash value at any time.

What's the difference between Relevant Life Insurance and Over 50s protection?

The main difference is that Relevant Life Insurance is a tax-efficient term policy, so it covers you for a specific amount of time, while over-50 life insurance is a whole of life policy, so it covers you for the rest of your life.

Typically to take out a Relevant Life Insurance policy you need to be aged between 18 and 77 to apply, and your coverage stops at the end of the policy term. You choose a cover amount, and if you want your cover to remain the same, be protected from the effects of inflation, or decrease over time broadly in line with a repayment mortgage or loan. You can take out a single or joint life insurance policy.

If you’re not sure which one might be right for you, speak to a Broadbench financial adviser.

What’s the difference between Relevant Life and Life Insurance?

Life Insurance is cover that you pay for with your own money. However, if you are set up as a limited company, you can pay for your Life Insurance through your business, as a tax-deductible expense, saving you 20%. This is known as Relevant Life Insurance.

How can I set up a Relevant Life Insurance policy?

If you’re looking to set up your Life Insurance, our advisers can help you find the right policy for you and your family. Get in touch.

Personal Protection

IHT Planning

Who pays UK Inheritance Tax?

Inheritance Tax (IHT) applies to all UK domiciles, regardless of whether they live in the UK or abroad, subject to the nil-rate band. There is no IHT due on estates valued under £325,000.

What Is a UK Domicile?

Your domicile is typically determined by your father’s domicile at birth (or mother’s, in some cases). This means that even if you were born outside the UK or live abroad, your domicile is linked to your father’s domicile. Living abroad does not automatically change your UK domicile status.

Which assets are subject to Inheritance Tax?

IHT applies to worldwide assets, including property, savings, investments, and other valuables. Some reliefs may apply, such as business relief and agricultural land relief, which can reduce the amount of tax owed.

How does UK domicile affect IHT?

UK domiciles are liable to pay Inheritance Tax on their worldwide assets. Even if no IHT is due, beneficiaries must report assets to HMRC. Gifts made more than 7 years before death are generally exempt from IHT, but be aware that IHT legislation may change, so it’s always best to consult your Broadbench financial adviser.

Do expats pay IHT?

Yes, if you are a UK domiciled individual, you are required to pay IHT regardless of where you live. You may also face local inheritance taxes in your new country of residence. To avoid being taxed twice, it’s advisable to check for double tax treaties between the UK and your new country.

How much Is UK IHT?

UK IHT is charged at 40% on estates valued over the £325,000 threshold. However, certain exemptions and reliefs can apply, such as the 36% rate if 10% of the estate is donated to charity.

Are there allowances against IHT?

Each individual has a nil-rate band (NRB) of £325,000, meaning no tax is due on the value of the estate up to this amount. Married couples or civil partners can combine their NRBs, effectively doubling the allowance to £650,000.

How do spousal exemptions work?

Spouses or civil partners can transfer assets tax-free between each other, with no limit on the value of assets. However, the recipient must be UK domiciled to benefit from this exemption.

Is IHT avoidable?

IHT is often referred to as a “voluntary tax” because there are legal ways to reduce it. Strategies include gifting, using trusts, claiming exemptions, and planning with tax-efficient financial instruments. A professional adviser can help guide you through these strategies.

Who pays IHT?

The executor of the estate is responsible for managing the payment of IHT before distributing assets to the beneficiaries.

Do I need to change domicile to avoid IHT?

No, you do not need to change your domicile to avoid IHT. There are other tax-efficient strategies that can be employed. Changing domicile is complex and could revert if you return to the UK. The best approach is to develop a tailored estate strategy with the help of a financial adviser.

How to value an estate for Inheritance Tax

To determine if IHT applies, you must first estimate the total value of your estate. If it exceeds £325,000, a more detailed valuation is needed.

The estate value includes:

- Assets you own, such as property, savings, investments, and cash.

- Assets held in trust (relevant property) where you are the beneficiary.

- Lifetime gifts made in the last seven years.

- Foreign assets held abroad.

Once you have the total value, subtract any debts (mortgages, loans) to arrive at the estate’s net value. If it exceeds the threshold, IHT will be due.

Use our IHT calculator above as a guide.

What should I consider before making lifetime gifts?

Lifetime gifts can be a strategy to reduce IHT, but there are several considerations:

- Ensure compliance with the rules.

- Be cautious about gifting if it leaves you financially vulnerable later in life (e.g., for care costs).

- Consider whether you want to retain control over how and when beneficiaries receive gifts. For example, using trusts can allow you to specify when beneficiaries can access the assets.

Who pays Inheritance Tax on gifts?

Gifts made during your lifetime are considered part of your estate for IHT purposes. If their value exceeds the available IHT allowances, the beneficiaries of the gifts are responsible for paying 40% IHT on the excess, even if the gift has already been spent or sold.

Does Equity Release effect Inheritance Tax?

Equity release allows you to access money tied up in your home, which can reduce the overall value of your estate, potentially lowering your IHT liability. However, this strategy can have long-term financial consequences, so it’s important to seek professional advice.

Buildings and Contents

What does "new for old" mean?

“New for old” means that if you make a claim, your insurance provider will replace the damaged or stolen item with a brand-new one of the same make and specification. However, this does not apply to clothing and household linen, where a deduction for wear and tear is made.

How do I calculate the rebuilding cost of my property?

The rebuilding cost of your home is not the same as its market value. It represents the amount needed to completely rebuild your home, excluding the value of the land.

You can check your current home insurance documents, surveyor’s report, or mortgage valuation (if done in the last two years) for the rebuild cost. Alternatively, you can use the BCIS rebuild calculator for an estimate: BCIS Rebuild Cost Calculator.

What is the policy excess?

An excess is the portion of a claim you are responsible for paying before your insurer covers the rest. The higher the excess you select, the lower your premium. You can adjust your excess amount at any time.

Some claims have specific excess amounts, such as a £1,000 excess for subsidence, heave, or landslip claims, which will be detailed in your policy schedule.

Will my insurance cover items away from home?

Yes, but only if you have selected the appropriate cover. The following optional add-ons provide protection for personal items outside the home:

- Personal Items – Covers valuables such as jewellery and handbags.

- Technology & Entertainment – Covers gadgets, laptops, and tablets.

- Pedal Cycles – Covers bicycles.

Check your policy schedule to confirm what is included.

Does home insurance cover wear and tear?

No, home insurance covers sudden and unexpected damage. It does not cover items that have naturally worn out over time, broken down, or been poorly maintained. Keeping your home and possessions well-maintained is essential, as insurance is not a substitute for proper upkeep.

What is not covered by my home insurance policy?

Exclusions vary by policy, but all important exclusions will be outlined in the “What is not covered” section of your policy documents. Reviewing these details ensures you fully understand your coverage.

Do I need Landlord Insurance?

If you rent out a property, standard home insurance may not be enough. Landlords face additional risks, such as:

- Tenant-related damage

- Loss of rent

- Liability claims from tenants

By informing us that your property is rented out, we can tailor a policy to suit your needs.

What does landlord insurance cover?

Landlord insurance covers typical home insurance risks, plus additional protections designed for rental properties, including:

- Loss of rental income if tenants can’t stay due to damage.

- Alternative accommodation costs for tenants if your property becomes uninhabitable.

- Property owner’s liability in case a tenant or visitor gets injured.

What doesn’t landlord insurance cover?

Each policy will have specific exclusions, which are listed in your policy documents. Reviewing these details will help you understand the limits of your coverage.

How much does landlord insurance cost?

The cost of landlord insurance depends on several factors, including:

- Property location and size

- Construction type

- Number of tenants and property use

- Level of cover selected

For an accurate quote, it’s best to discuss your specific needs with an adviser.

What landlord insurance do I need?

We offer a variety of landlord insurance policies to suit different needs, including:

- Residential landlord insurance – For properties rented to individuals or families.

- Commercial landlord insurance – For business premises you lease out.

- Mixed-use landlord insurance – For properties with both residential and commercial tenants.

- Portfolio landlord insurance – For multiple rental properties under one policy.

Does contents insurance cover accidental damage?

Standard contents insurance does not always include accidental damage cover. However, you can add this as an optional extra to protect against incidents such as spilt drinks on furniture, broken electronics, or damaged carpets.

Are high-value items covered under contents insurance?

Most policies have a single-item limit, meaning high-value items such as expensive jewellery, art, or antiques may need separate coverage or specified item listing in your policy. Check your policy’s coverage limits or speak to an adviser to ensure full protection.

Whole of Life

What is Whole of Life (WOL) insurance?

Whole of Life insurance provides a guaranteed payout when you pass away or are diagnosed with a terminal illness. It’s often used to leave a financial legacy for family, pay off debts like a mortgage, or cover funeral costs. You can choose the level of cover that best suits your needs, but this type of policy is only available through a financial adviser.

What happens if I stop making payments?

Whole of Life insurance has no cash-in value at any point. If you stop paying your premiums, your cover will end immediately, and you won’t receive any refunds or payouts.

Why should I go through a financial adviser?

A Broadbench financial adviser can help tailor a policy that meets your unique needs and budget. Their expertise ensures you get the most suitable cover, helping you avoid unnecessary costs or gaps in protection.

Can I take out a joint Whole of Life insurance policy?

Yes, joint Whole of Life policies are available. They are typically more affordable than two separate policies but usually pay out only once—either when the first person on the policy passes away or, in some cases, upon the second death, depending on the type of policy chosen.

Are Whole of Life insurance payouts tax-free?

Life insurance payouts are usually subject to inheritance tax (IHT) at 40%, as they are included in your estate.. Find out more about IHT Planning.

However, by placing your policy in a trust, the payout can be kept separate from your estate, reducing or eliminating tax liability. Speak with an adviser to ensure your policy is set up correctly for tax efficiency.

Can I get whole of life insurance if I’m over 50?

Yes, Whole of Life insurance is available for those over 50. While premiums generally increase with age, many insurers offer competitive rates for older applicants. An adviser can help you find the best deal based on your circumstances.

Can Whole of Life insurance include health coverage?

Some Whole of Life policies include critical illness cover, which provides a payout if you’re diagnosed with specific medical conditions during your lifetime. This can offer additional financial security in case of serious illness.

Is Whole of Life insurance available for diabetics?

Yes, diabetics can qualify for Whole of Life insurance, though premiums may be higher. However, Broadbench advisers specialise in finding affordable policies for individuals with diabetes. If you’re diagnosed after taking out your policy, your original premiums will typically remain unchanged.

What if I no longer want Whole of Life insurance?

Some policies allow you to surrender your plan for a cash value, though exit charges or penalties may apply. However, not all Whole of Life policies offer this option, so it’s essential to check the details before purchasing.

How much Whole of Life cover do I need?

Your coverage should account for:

- Outstanding debts (mortgage, loans, credit cards).

- Income replacement to support dependents.

- Future expenses, such as university fees for children.

Online life insurance calculators can help, but working with an adviser ensures you select the right level of cover for your needs.

When is the best time to buy Whole of Life insurance?

Life insurance is cheaper the younger and healthier you are. Whole of Life policies often include a savings element, which can grow over time, making it beneficial to purchase as early as possible.

Life Insurance

What is Life Insurance?

It’s not a nice thing to think about, but if you’re a contractor and you pass away, how would your loved ones survive? This is where Life Insurance can provide the answer. It pays out a large one-off sum to help your family live after you’ve gone.

Do I get any money back if I don't die before the Life Insurance Policy term ends?

No. There’s no cash value at any time. At the end of your Life Insurance policy term, you stop making payments and your cover ends.

Can my mortgage be covered with Life Insurance?

If you have an interest-only mortgage, your outstanding mortgage loan stays the same until you repay it at the end of the mortgage term. Level Life Insurance could cover this type of mortgage.

How does Life Insurance work? What do I need to know?

It provides your loved ones with a large tax-free, one-off payment, or monthly payments if you pass away. It can be used to pay the mortgage off or help your family with living expenses. Monthly payments are tax-deductible if you are a limited company – look at Relevant Life Insurance. You are covered only for the duration (term) of the policy and cover only lasts while you keep up monthly premiums. Monthly payments can be reduced by combining this with a Critical Illness policy.

How do I know what the right policy for me is?

If the unexpected happens, you’d want your family to be taken care of. You’d want the mortgage paid off and enough money for them to live. It’s important to get this right, which is why we work closely with you, making sure the cover fits your needs but is also affordable for you. The policies we recommend are handpicked for business owners, professionals and contractors, and we’ll cut through any jargon, so you know exactly where you stand.

Will my payments on my Life Insurance policy change?

If you choose level or decreasing cover, your monthly payments are guaranteed to stay the same for the duration of your policy.

For decreasing Life Insurance, premiums are set at the start of the policy to consider the decreasing amount of cover you’ll need during the policy term. Premiums for decreasing cover are often cheaper than other types of life insurance.

With level cover, if you choose to help protect your payments from the effects of inflation, so the lump sum won’t be worth less in the future, your monthly payments may rise.

With index-linked cover life insurance, your death benefit increases over the life of the policy. This type of insurance can provide extra protection as the years go by to cover growing expenses, like a new house or bigger family, or protect your death benefit from inflation. The advantage of increasing/ index linked cover term insurance is that you don’t have to predict inflation – the policy will do this for you, but at a cost. Also, your increases are automatic and won’t be hindered if your health changes.

I have a mortgage. Do I need Life Insurance?

If you have a mortgage, you might want to take out Life Insurance. Then, if you die before your policy ends, the lump sum can be used to help pay off the outstanding mortgage balance, so your family could stay in their home. Some lenders will ask you to take out Life Insurance as part of their mortgage offer.

Do I have to take out decreasing Life Insurance to cover a mortgage?

No, you don’t have to take out decreasing Life Insurance to cover a mortgage. The reason for the policy depends on a few factors, such as what you want the lump sum to cover, and how much you want to pay each month. We will advise you on the different levels of cover to suit different needs, so you can choose which one is right for you and your family.

Who do I notify in the event that a policyholder passes away?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

What do I do if I change my name?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

I've moved house, how do I update my address details for my Life insurance policy?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

What should I do if my bank details change for my Life Insurance policy?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

Can I cancel my Life Insurance policy at any time?

Yes. You have a 14-day cooling-off period from your policy start date, or from when you get your policy documents (whichever is later), to change your mind. If you want to cancel within this time, we’ll refund any premiums you’ve paid. Remember, there’s no cash value and, if you cancel your policy, you won’t be able to make a claim.

How do I pay for my Life Insurance policy?

You can pay your premiums monthly by Direct Debit.

Is my Life Insurance linked to my mortgage?

We can’t directly link your Life Insurance plan to your mortgage. However, your mortgage lender may register an interest in a portion of the proceeds to cover the remaining cost of the mortgage if you were to die before it’s repaid. But this only acknowledges a third-party interest, and your cover amount still won’t be directly linked to whatever’s left to pay on your mortgage.

Is Terminal Illness Cover included in a Life Insurance policy?

Many Life Insurance policies have the option to include Terminal Illness Cover. Your Broadbench adviser will go through all of the available options with you to ensure the policy meets all of your requirements.

What does my Life Insurance policy cover me for?

You can find out what you’re covered for in the policy documentation. If you’re not sure please contact us.

What’s Life Insurance with decreasing cover?

If you have a Life Insurance plan with decreasing cover, the cover amount decreases over time, broadly in line with the repayment mortgage or long-term loan that you’re repaying. Your premiums stay the same during the term of the policy, unless you make changes to the cover. Decreasing cover usually costs less than level cover.

The policy will pay out if you die, or are diagnosed with a terminal illness and aren’t expected to live longer than 12 months, during the policy term. The policy only pays out once and has no cash value at any time.

What’s Life Insurance with increasing cover?

If you have a Life Insurance policy with increasing cover, the level of cover, and your monthly payments, may increase over time to help protect your cover amount from the effects of inflation.

The policy pays out a lump sum if you die during the policy term, or are diagnosed with a terminal illness and aren’t expected to live longer than 12 months. The policy will only pay out once, so if you make a successful terminal illness claim, a second claim can’t be made. There’s no cash value at any time.

What is Terminal Illness Cover?

Terminal Illness Cover will pay out when you contract an illness/ disease that has no known cure or has progressed to a point where it cannot be cured, and you aren’t expected to live longer than 12 months.

What's the difference between Life Insurance and Over 50s protection?

The main difference is that Life Insurance is a term policy, so it covers you for a specific amount of time, while Over 50s cover is a whole of life policy, so it covers you for the rest of your life.

Typically to take out a Life Insurance policy you need to be aged between 18 and 77 to apply, and your coverage stops at the end of the policy term. You choose a cover amount, and if you want your cover to remain the same, be protected from the effects of inflation, or decrease over time broadly in line with a repayment mortgage or loan. You can take out a single or joint life insurance policy.

If you’re not sure which one might be right for you, speak to a Broadbench financial adviser.

What’s the difference between Relevant Life and Life Insurance?

Life Insurance is cover that you pay for with your own money. However, if you are set up as a limited company, you can pay for your Life Insurance through your business, as a tax-deductible expense, saving you 19% or more. This is known as Relevant Life Insurance.

How can I set up Life Insurance?

If you’re looking to set up your Life Insurance, our advisers can help you find the right policy for you and your family. Get in touch.

Private Healthcare

What is Private Healthcare?

No one likes being ill but, when you’re a business owner, professional or contractor and your income relies on your ability to work, it’s vital you get back on your feet as soon as possible. A Private Healthcare plan means that you and your family can have access to the best health facilities, without the wait times, so you can protect yourselves from any health issues (and subsequent financial strain) that might come your way.

What does Private Healthcare cover?

Private Healthcare plans are typically designed to cover acute medical conditions. This includes short-term illnesses, treatable diseases and injuries which, through care, you are likely to make a full recovery from. If you have an existing chronic condition, it’s likely that this will be excluded from any cover you take.

Why do I need Private Healthcare?

Unlike other forms of insurance, Private Healthcare tends to be viewed as optional. This is because we are fortunate to live in a country that offers an extensive National Health Service that will cover most treatments for free. However, due to long waiting lists and lack of choice, it could also benefit contractors to have Private Healthcare in place.

As a business owner, professional or contractor, if you can’t work, you can’t earn. With a Private Healthcare policy, you can rest assured that if you do have an illness or injury, you’ll be able to get back on your feet and back to work faster than usual.

Are pre-existing conditions covered?

Private Healthcare is designed to cover conditions that you may develop after taking out the policy. However, depending on the insurer, you may be able to cover pre-existing medical conditions. Keep in mind that this will have an impact on the cost of your premiums.

What are the benefits of Private Healthcare?

Getting help faster – Being seen quickly is one of the many reasons contractors consider Private Healthcare. If you’re unable to earn due to an illness or injury, Private Healthcare will get you back on your feet faster than regular NHS services. You may have access to better care as well as medication and treatments that are not yet available on the NHS.

Privacy and choice – By purchasing Private Healthcare you often have more choice and greater privacy. You may be able to choose a hospital or doctor and even request your own private room – this wouldn’t be available to you if you used the NHS.

What factors affect the premium?

There are many factors that can influence the cost of your premiums. Typically, your age, current health and medical history, but your job may also have an impact if it is seen as a risky profession. If you’re a smoker you may have higher premiums than non-smokers.

What’s important to consider when looking for Private Healthcare?

When looking to get a Private Healthcare policy, it’s important for you to understand what type of cover you require. Do you want comprehensive coverage (which will cover you for everything) or a policy that simply covers you for outpatient visits?

You may also need to consider what could be affecting the price of your premium. Getting the best possible cover won’t be the cheapest but you can’t put a price on your well-being when you’re a contractor. Therefore, it is best to speak to an adviser to find out the level of cover you need to suit you and your circumstances.

How can I set up a Private Healthcare policy?

When it comes to things as important as protecting our health and finances, we believe that you should receive the best impartial advice. To set up a Private Healthcare policy, or if you have more questions and want to speak to an expert, get in touch.

Who do I notify in the event that a policyholder passes away?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

What do I do if I change my name?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

I've moved house, how do I update my address details for my Private Medical Insurance?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

What should I do if my bank details change for my Private Medical Insurance?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

What are the benefits of Private Healthcare?

Getting help faster – Being seen quickly is one of the many reasons contractors, business owners and professionals consider Private Healthcare.

Who do I notify in the event that a policyholder passes away?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

Critical Illness Cover

What is Critical Illness cover?

Critical Illness cover (also known as Critical Illness Insurance) is a medium to long-term policy which covers you for a serious illness during the policy period so you don’t have to worry about your finances.

How does Critical Illness work?

If you are diagnosed with a serious illness, a Critical Illness policy will pay out a tax-free, one-off payment (some insurers may offer monthly instalment options also). This can help you pay for your mortgage or rent, and any existing debts you may have or help you to make adjustments to your home, such as a wheelchair ramp if you need it.

Why do business owners, professionals and contractors need Critical Illness?

When you work for yourself, you no longer receive the same benefits as regular employees. These benefits include payment to cover a long period off work due to sickness. The alternative to receiving ‘sick pay’ is to receive state benefits, however, this may not be enough to replace your income.

If you’re eligible, you may be able to receive Employment and Support Allowance (ESA) – which ranges from £70 to just over £100 a week, depending on your circumstances and the seriousness of your illness or disability. Will that be enough to cover your household bills and family’s lifestyle? If not, then you should consider Critical Illness cover.

What illnesses are covered?

Each insurer has its own list of critical illnesses that they cover. Typically, you’ll be insured for heart attacks, cancer (depending on the type and the stage), strokes and permanent disabilities due to an illness or injury. If you have a specific illness that you want to be covered for, get in touch with a Broadbench adviser who will be able to guide you to the right insurer.

What factors impact the policy’s cost?

There are a number of factors that can influence the cost of your monthly premium including:

- Your age

- The level of cover you wish to take out

- Whether you’re a smoker or have previously smoked

- Your current health, weight and family’s medical history

- Your job (some occupations carry higher levels of risk than other professions and therefore may increase the monthly premiums)

What are the benefits of Critical Illness Cover?

Firstly, to keep a roof over your family’s head. With Critical Illness Cover, you can rest assured that you will be able to keep up with mortgage repayments or even pay off the full remaining amount. You’ll receive a tax-free pay-out – If you are diagnosed with a Critical Illness, the money you and your family receive is tax-free. Lastly, it gives you peace of mind – No one knows what the future has in store but with Critical Illness Cover, you will be protected for a number of illnesses. This way you can rest assured that you and your family are financially secure.

You may be able to get small multiple payouts. Most policies will only pay out once, but some insurers will make a small payment if you are diagnosed with a less severe illness. In this case, your policy would continue, and you should be able to make a further claim down the line if you’re diagnosed with a more critical illness.

How is Critical Illness different from Income Protection?

To claim on a Critical Illness policy, you must be diagnosed with a medical condition that meets one of the definitions on the policy. In contrast, to make a claim on an Income Protection policy simply relies upon you being unfit for work, no specific medical condition is needed – therefore the pay-out is to cover you until you’re fit to return to work.

How can I set up a Critical Illness policy?

When it comes to things as important as protecting our health or finances, we believe that you should receive the best advice. To set up a Critical Illness policy, or if you have more questions and want to speak to an expert, get in touch.

Who do I notify in the event that a policyholder passes away?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

What do I do if I change my name?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

I've moved house, how do I update my address details for my Critical Illness Cover?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

What should I do if my bank details change for my Critical Illness Cover?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

Why do contractors need Critical Illness?

When you work for yourself, you no longer receive the same benefits as regular employees. These benefits include payment to cover a long period off work due to sickness. The alternative to receiving ‘sick pay’ is to receive state benefits, however, this may not be enough to replace your income.

If you’re eligible, you may be able to receive Employment and Support Allowance (ESA) – which ranges from £70 to just over £100 a week, depending on your circumstances and the seriousness of your illness or disability. Will that be enough to cover your household bills and family’s lifestyle? If not, then you should consider Critical Illness cover.

Income Protection

What is Income Protection Insurance?

Income Protection is an insurance policy that pays you a regular wage if you’re unable to work due to illness or injury. It will continue to pay you a salary until you’re ready to return to work, retire or if you pass away (dependent on the level of benefit taken).

What does Income Protection cover?

You are covered for most injuries or illnesses, unlike other protection policies. The criteria for a claim within an Income Protection policy is not based on the illness/injury itself but on whether it has stopped you from working.

Will Income Protection protect me if I can’t find a contract?

No. This is a common misconception of Income Protection; it only covers you when you are unable to work due to illness or injury. It does not cover gaps in between employment. If you’re looking for unemployment payment, you will have to apply for JSA.

How much of my pay will be protected?

As a contractor, you can typically ensure between 50% – 80% of your salary and dividends.

What factors impact an Income Protection premium?

Your age, health, line of work and if you have smoked in the last 12 months can have an impact on your monthly premium. Therefore, it’s important to speak to an Income Protection expert to get a rough idea of what cover you can expect and at what cost before applying.

Why is it important for those earning a day rate to have Income Protection?

When you work for yourself, you do not have the financial support of an employer. This means that if you fall ill and are unable to work for a period of time, you do not benefit from sick pay. If this happens, how will you meet your living costs? It’s important to have an Income Protection policy in place so you can meet your living costs (mortgage, bills, food, lifestyle etc) in the unfortunate circumstance of illness or injury.

How long should my deferred period be?

The deferred period is the time between you being unable to work and your payouts beginning. Typically, the longer the deferred period the lower your monthly premiums. To work out the length of your deferred period, you should consider how much you need per month to cover your bills and day-to-day living costs and offset this against your savings. From this, you can work out how long your savings will keep you afloat before you’ll need the financial support a policy delivers.

What happens if I change contracts?

If your new contract pays more or less than the previous contract (or the contract you were on when you started the policy), you can contact your insurer to increase or decrease the amount of coverage you need.

How long can I be covered for?

There are two forms of Income Protection: short-term which typically covers you for 2-5 years and long-term. Long-term will cover you up until an agreed age (usually until retirement). Most contractors take out a long-term policy so that they can be confident they’ll be financially supported in the event of long-term illnesses and injuries.

What do I do if I change my name?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

I've moved house, how do I update my address details for my Income Protection?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

What should I do if my bank details change for my Income Protection?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal. Your new Direct Debit will be active within 14 days.

Why do I need Income Protection Insurance?

People in permanent jobs have the benefit of receiving sick pay. Those earning a day don’t have this luxury which is why it’s so important to have Income Protection. It gives you the peace of mind that if you become ill, you’ll be paid a regular wage so you can look after the bills until you’re well enough to return to work.

Can I get Income Protection Insurance if I am self-employed?

Yes, although it’s structured to be paid for personally rather than via a Limited Company.

Who do I notify in the event that a policyholder passes away?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

How can I set up Income Protection?

If you’re looking to set up your Income Protection, our advisers can help you find the right policy for you and your family. Get in touch and protect your income!

Mortgage Advice

Further Advance

What is a Further Advance?

A Further Advance is additional borrowing from your current mortgage lender, secured against your home. It allows you to access extra funds without remortgaging or switching lenders.

How is a Further Advance different from a remortgage?

With a remortgage, you switch your mortgage to a new lender (or a new deal with the same lender), often paying fees and legal costs. A Further Advance lets you borrow more from your existing lender without moving your mortgage.

Who can apply for a Further Advance?

Eligibility depends on your lender, your property’s value, and your financial situation. Typically, you must have a good payment history, meet affordability checks, and have enough equity in your home.

How much can I borrow?

Lenders usually have a maximum Loan to Value (LTV) limit, often around 80–85% of your property’s value. The exact amount depends on your existing mortgage, income, and credit profile.

Will the Further Advance affect my current mortgage rate?

The additional borrowing may have a different interest rate or terms from your original mortgage. Your adviser can help you understand the new monthly payments and overall cost.

What can I use a Further Advance for?

Common uses include home improvements, consolidating high‑interest debt, funding education costs, or other large expenses. Lenders typically don’t restrict the purpose, but some may have specific rules.

Are there any fees or costs?

Some lenders charge an arrangement fee, valuation fee, or legal costs for a Further Advance. These are usually lower than the fees for a full remortgage, but it’s important to check with your lender.

How long does it take to get a Further Advance?

Once you’ve submitted your application and the lender has completed affordability checks and any required valuation, it usually takes a few weeks. Times can vary depending on the lender.

Can I get a Further Advance if I have a fixed‑rate mortgage?

Yes, but the Further Advance may be on a separate rate or term from your existing fixed rate. Your adviser can explain how this impacts your monthly payments and interest.

Is a Further Advance right for me?

A Further Advance can be a cost-effective way to borrow more, but it isn’t suitable for everyone. You should consider affordability, future plans, and alternative options like remortgaging or a second charge loan. Your Broadbench mortgage adviser can help assess what’s best for your situation.

Remortgages

What is remortgaging?

Remortgaging is the process of switching your existing mortgage product to a new mortgage product, either with your existing lender or a new lender.

What happens when my fixed-rate mortgage deal comes to an end?

If you’re currently on a fixed rate mortgage, it means for a period of time (typically between 2-5 years) the interest you pay and the monthly repayment will be fixed. Once your fixed mortgage deal comes to an end, you will be placed on the ‘Standard Variable Rate’ (SVR). Each lender sets their own SVR and it tends not to be as competitive as fixed-rate mortgages.

I was permanent when I took out my mortgage but now I am earning a day rate. Will I be accepted for a remortgage as a contractor?

You will still be able to get a mortgage however, your existing lender might not be able to understand your income now you’re contracting. It’s important to speak to a specialist contractor mortgage adviser who works with the whole of market and will find a lender that can understand your income and make sure you’re getting the best mortgage product available.

How much could I save by remortgaging?

It’s important to speak to a specialist mortgage adviser who works with the whole of market.

What documents do I need to remortgage?

If you’re switching to a new lender, the documents you need to provide will be similar to when you applied for the first mortgage. This will include details of your current and previous contract (if applicable), 3 months’ bank statements and if you have less than 3 months remaining on your contract, they will require a contract extension.

Are there any charges for remortgaging?

There are some fees to be aware of when remortgaging, for example, some lenders have upfront product fees that can be added to the loan, usually about £1000. Lenders do offer a free legal and valuation service to help you switch. If you’re not sure whether you’d want to pay a product fee, a mortgage specialist can help you look through the options.

Can I borrow more by remortgaging?

A great benefit of remortgaging is that it gives you an opportunity to borrow more money. This can be used to make home improvements such as building an extension or refurbishing the kitchen or bathroom. Make sure you speak to an expert mortgage adviser to help assess how much you can borrow based on your day rate.

Where can I find the best rate?

This is where we can help. Scouring the market for the best mortgage product can be a long and difficult process and, unless you have the right expertise, you may not end up with the best deal for you. Our specialist mortgage advisers do all the leg work, working with contractor-friendly lenders, so you don’t have to. Speak to your Broadbench adviser and see how much you could save on your remortgage.

What's the difference between remortgaging and a product transfer?

A remortgage involves switching to a new mortgage deal, potentially with a different lender, while a product transfer involves switching to a new deal with your current lender.

Fees:

- Product Transfers (remaining with your existing lender): No fee

- Remortgages (moving to a new lender): £250 arrangement fee (a reduced rate for existing clients)

Buy to Let

What is a Buy To Let mortgage?

A Buy to Let mortgage is where you buy another property specifically as an investment with the intention of letting it out.

How much deposit do I need for a Buy to Let mortgage?

Normally a minimum of 25% deposit.

Is there any tax to pay when I sell my property?

Not for your main residence, but if you have investment properties that were bought on a Buy to Let basis, these will be subject to Capital Gains Tax. Other taxes may also be levied, we recommend you speak with an accountant to establish your tax position.

Can I get a mortgage if I earn a day rate, rather than PAYE?

Yes. Of course, there are factors that impact a contractor’s eligibility, but just by being self-employed, you should not expect to be turned down by a lender as long as they understand contractors and contracting. However, factors that would prevent anyone from securing a mortgage, such as a poor credit history or a bad payment record will apply just as much. to contractors as to employees.

Can I get a mortgage if I have only just started contracting?

Yes! As long as we can see you’ve got a history in the same line of work and in the same industry in which you are now contracting, there are lenders who accept new contractors.

What is the Mortgage process?

A typical journey will look like this:

- Welcome Call

This is an introductory meeting. You’ll meet your Broadbench adviser: they’ll explain our services, our regulatory status and establish a basic understanding of your requirements. - Fact-find

Your adviser will send you a fact-find document for you to complete. Once received, your adviser will schedule a Discovery Call. - Discovery and Recommendation Call

We’ll confirm the details supplied in the fact-find, and discuss your mortgage options: fixed/tracker, term, fees, and your budget. Your adviser will also advise you about life insurance products to protect the mortgage and your family’s lifestyle.Your adviser completes your mortgage recommendation and the KFI (Key Features Illustration) and then will advise you on the AIP process. You’ll both agree what are the next steps: house hunting or booking your mortgage. - AIP (Agreement In Principle)

Your adviser will send you an invoice of £100 to create the AIP. Once payment is received the AIP can be booked. - Documentation

Then adviser will send you a checklist of all the documentation you need to supply to us. You’ll then be invoiced for the remaining £400. - Mortgage Offer

Once all documents are received, we’ll certify that your mortgage is ready to be booked. Your adviser then books your mortgage. Once the mortgage offer is received, we’ll liaise with the lender on your behalf. - Mortgage Review

You let us know your exchange and completion dates. - Mortgage Completion

We’ll let you know as soon as your mortgage completes and then schedule regular reviews during the mortgage term to ensure that the product remains the most suitable for you.

Why should I use a specialist broker?

By all means, go to a high street lender to satisfy your curiosity, but in most cases, the lender will have issues with how income reaches the contractor. High street lenders understand dividends, but business owners, professionals and contractors who are tax efficient and only draw down a minimum salary and dividends to meet their needs won’t look good. Specialist brokers like us go to the same lenders you see in the high street but at the head office underwriter level. This means they are speaking to people with a bigger lending mandate and a knowledge of this sector contractors, and they use the contract to define a contractor’s income.

Home Mover

Why should I use a specialist Contractor broker?